Avoiding Common Mistakes

While there is general agreement that reducing inventory levels is beneficial, there does not seem to be consensus on how to value a reduction in inventory. Whether it’s from my university students or corporate managers and executives, I frequently see business cases associated with inventory reduction projects that grossly misrepresent the benefits associated with that reduction. At best these undervalue the benefits, but in many cases the errors would cause an incorrect decision about the initiative or investment in question. Every situation is different, but I would like to lay out what I believe is the correct approach and framework for building an inventory reduction business case – one that puts the right variables in focus to drive good decisions.

I believe that the primary reason that many people and companies struggle with business cases around inventory is that, fundamentally, inventory is about cash flow where most supply chain business cases are about cost reduction. This leads to the first of the common mistakes that I see:

Common Mistake #1: Focusing the business case on costs and ignoring cash impacts

The desire to focus on costs is very natural, after all it’s what we do in most other supply chain business cases. And almost any action that impacts inventory will also impact cost elements, like warehousing and obsolescence, in addition to implementation costs. This often creates a desire to convert the change in inventory to a set of cost impacts – with cost of money being one – and ignore the direct cash flow impacts. This is particularly true when there is a desire to hit a cost reduction target.

Many businesses use Net Present Value (NPV), Internal Rate of Return (IRR) or other Return on Investment (ROI) metrics to evaluate business cases. While the focus is often on measuring the impact of changes in costs, these metrics are actually intended to measure changes in cash flows. Consequently, excluding the favorable cash flow generated by a reduction in inventory would significantly understate the value of such a change. The cost of money is reflected in the discount rate used to calculate NPV. So, to include cost of money as a cost reduction is inappropriate as it effectively double counts those benefits.

A reduction in inventory generates a one-time favorable cash flow, as long as the inventory is sold or otherwise consumed and not scrapped. The same reduction also creates an on-going reduction in the costs associated with holding inventory, such as the risk of loss or obsolescence and the costs of storage. Assessing those costs can be a little tricky, and I will discuss that in more detail below. However, the bottom line is that a business case for inventory reduction is fundamentally about the cash flow impacts, and can’t be viewed solely through a cost reduction lens.

Inventory is primarily a cash flow benefit

Inventory reduction creates a one time cash benefit

Common Mistake #2: Treating inventory reduction as a recurring benefit

When considering cost reductions, if a cost is reduced and stays reduced, it delivers benefit not only in the year of reduction but in each year after that. So if inventory is reduced and remains reduced, wouldn’t the inventory reduction continue to deliver benefits in subsequent years? The answer is yes, and no. When inventory is reduced, the cash flow benefit occurs only once – at the same time as the inventory reduction. However, the cost savings associated with maintaining that inventory do recur. For example, let’s say I have a plan to eliminate 100 pallets of inventory with a value of $ 1 million. This inventory is stored in a public warehouse that charges $12 per pallet per month. When the inventory is eliminated, there is a one-time favorable cash flow of $1 million. This cash flow occurs at the time of inventory reduction. If the inventory is reduced say, $ 700,000 in Year 1 and $ 300,000 in Year 2 then there would be corresponding cash flows of $ 700,000 in Year 1 and $300,000 in Year 2. And nothing afterward. Note that the second year only shows the incremental benefit that occurs in that year and not the cumulative amount. It would be incorrect to show the total benefit of $ 1 million in any later years because this benefit only occurs once.

Now, with an average value of $ 1 million / 100 pallets = $ 10,000 per pallet these numbers would correspond to a reduction of 70 pallets in Year 1 and 30 pallets in Year 2. With a storage cost of $12 per pallet per month this would generate a savings of $ 10,080 in the first year (assuming the inventory was all reduced in January) and an incremental $ 4,320 per year in Year 2. These cost savings are both cumulative and recurring. So while the first year savings is only $ 10,080, the savings in Year 2 and beyond are $ 14,400 (10,080 + 4,320). Storage isn’t the only cost that might be reduced, but it will suffice for this example. Other elements of holding cost should be treated the same way

Common Mistake #3: Failing to properly consider holding costs

In the example above, I used storage cost to illustrate a recurring cost that might be reduced as a direct consequence of a reduction in inventory. Clearly, a reduction in inventory can reduce costs elsewhere and these cost impacts [1]should be considered as part of the overall business case for inventory reduction. Very often I see these impacts either left out or not treated properly. A business case should address all of the costs that will change as a result of the decision being evaluated – and nothing else. With the exception of those cases contemplating strategic or structural changes, a business case should be developed on a marginal basis with the status quo as a starting point. The challenge then is to identify those margin changes.

We have already discussed the cost of capital. While less inventory reduces the cost of money, it is not appropriate to include this as a cost savings. Rather, the cost of money is addressed through the discount rate in the NPV calculation. That leaves us with a number of other areas to consider:

- Storage/warehousing costs

- Obsolescence

- Shrinkage

- Taxes and Insurance

- Inventory management costs

Storage is perhaps the most tricky of these. In the example above, inventory was in a public warehouse that charged a flat monthly fee for each pallet in storage. In cases like this, any reduction in the number pallets would deliver a reduction in cost. However, most companies find themselves in a more complex situation with a mix of owned and contract warehousing. Depending on the business case, it also may be necessary to consider inventory that is “stored” in-transit in trucks or ocean containers or that is on the factory floor. This is where the concept of marginal analysis is critical. If you have an owned warehouse that is 95% full, then reducing inventory so that it is only 80% full will not reduce the cost of operating the warehouse. This is because the cost of the warehouse is largely fixed, and driven by the level of activity – not by the level of inventory[2]. If on the other hand, the owned warehouse is full to the point where off-site overflow storage is being utilized then there may be a clear savings if the off-site location can be downsized or eliminated. There may also be an opportunity to eliminate the cost of transporting inventory to the secondary warehouse and bringing it back. With respect to storage costs, it is important to ask exactly what costs will be reduced or eliminated based on the change being proposed. If you are reducing inventory in-transit or work-in-process it may very well be that the answer is that there is no impact to storage costs. What is required here is a thoughtful process to understand exactly what, if any, costs will be altered by the decision.

Storage costs may be the trickiest, and in my experience the most frequent source of error, but a similar process is needed for other components of holding costs as well. Understand the impact of the inventory reduction, think through the impacts on the drivers of other costs, and include the appropriate amount. In the case of both shrinkage and obsolescence[3] costs, it’s important to consider where the inventory is in the supply chain. How do loss, damage, or yield rates vary along the supply chain? Exactly what inventory is being reduced, and what rate applies to that inventory? Similarly with obsolescence, raw materials and components in the upstream portion of the supply chain tend to have much lower obsolescence rates than downstream inventory sitting in distribution centers. Taxes and insurance should be treated similarly.

As a general rule, the cost of managing inventory (people and systems) does not change due to the level of inventory. Rather it is driven by the number of stock keeping units (SKU’s) that need to be managed. However, if the source of the inventory reduction is a product portfolio rationalization, then it may be appropriate to include a component of these costs.

[1] See How is Holding Cost Calculated for more detail

[2] I will be quick to acknowledge that a very full warehouse leads to inefficiencies and there may be labor savings from creating a certain amount of free space in a full warehouse. These should absolutely be considered if they exist.

[3] For purposes of this discussion, think of obsolescence as anything that renders the product unsaleable. This would include perishability as well as the traditional notion of the product becoming obsolete for lack of demand.

Inventory reduction can also reduce on-going costs relating to holding and managing inventory

A Simple Example

A Simple Example

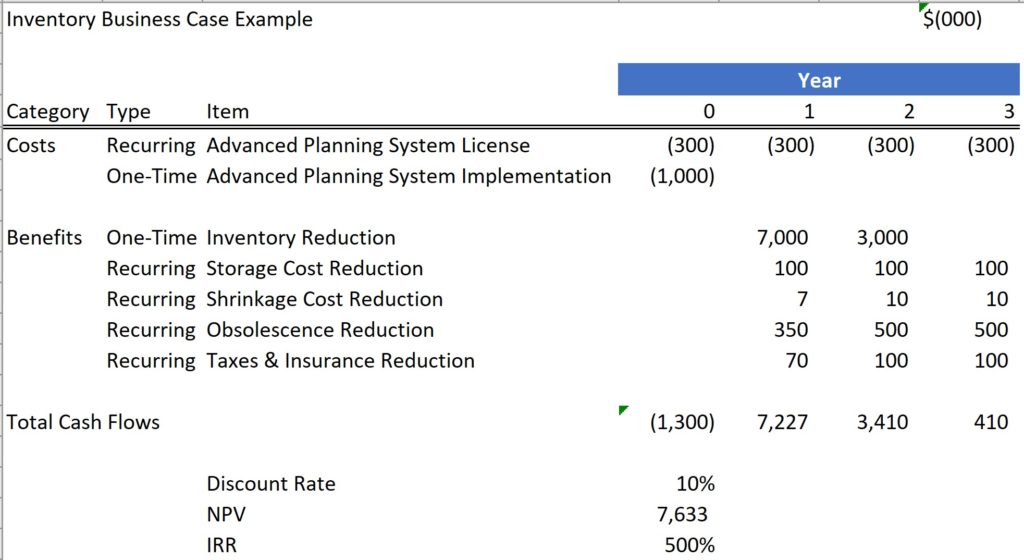

Perhaps the best way to illustrate the right way to do an inventory business case is with a simple example. It has been proposed to implement additional functionality in the planning system to better manage inventory. This requires new software which will have an annual license fee of $300,000 and an initial implementation cost of $ 1 million. It is expected that the new software will deliver a $ 10 million reduction in inventory over two years, with $ 7 million in the first year after implementation and an additional $ 3 million in the second year. The initial $ 7m reduction will allow the company to exit an overflow warehouse with cost savings of $ 100,000 annually. Inventory in this location typically incurs shrinkage of 0.1% annually and obsolescence / perishability of 5% annually. Taxes and insurance are 1% annually.

With this information, a correct business case would look like this:

Note that each element has been labeled as to whether it is on-time or recurring. As noted above, the full savings in storage costs occurs with the first $ 7m inventory reduction. The other holding cost elements ramp up in line with the cumulative savings in inventory ($7m reduction in Year 1, $ 10m reduction in Year 2).

All in, this is a very attractive business case with a 500% internal rate of return (IRR), and a net present value of over $ 7m.

The spreadsheet shown above can be found here: Inventory Business Case Example